Car Insurance First Month Free No Deposit

Company Trusted For Over 25+ Years*

Call us 1-855-371-6683

Company Trusted For Over 25+ Years*

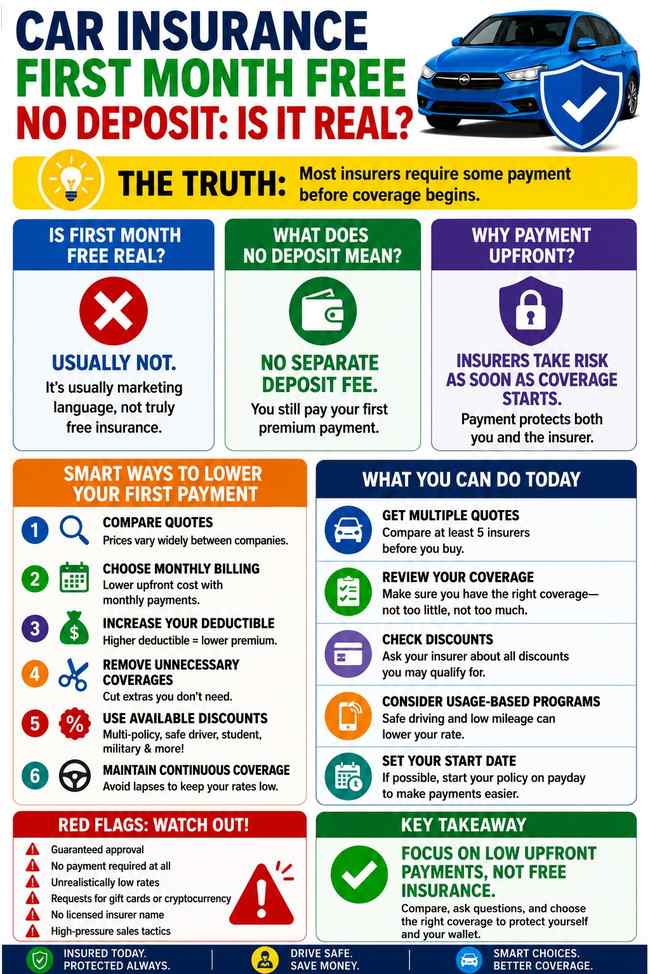

With rates hitting record highs, many drivers are searching for car insurance for the first month free with no deposit. The reality is that insurers usually require some initial payment before a policy is activated, but some options can get you covered for little money upfront.

Thousands of drivers look for ways to get insured without making a large upfront payment. Maybe money is tight, maybe you just purchased a vehicle and need proof of insurance today, or maybe your current policy is about to expire. When you see ads promising “first month free car insurance” or “no deposit auto insurance,” it can sound like exactly what you need. Unfortunately, many of these offers do not mean what consumers think they mean.

Most legitimate insurance companies require an initial payment before coverage begins. In most cases, first month free car insurance is not truly free, no-deposit insurance does not usually mean zero payment, coverage starts only after payment is received, and monthly payment plans can reduce upfront costs. The key is understanding the difference between marketing language and how insurance actually works.

Many consumers assume “first month free” means they can buy a policy today and make no payment for the first 30 days. That is usually not how legitimate vehicle insurance works.

Instead, the phrase may refer to:

Once you click through and obtain a quote, you’ll often discover that a payment is still required before coverage becomes active.

| Term | What Consumers Think | What It Usually Means |

|---|---|---|

| First Month Free | No payment for 30 days | Marketing language or promotional billing |

| No Deposit Insurance | Pay nothing today | No separate security deposit |

| Zero Down Insurance | Start for free | Rarely available from major insurers |

| Monthly Billing | Small upfront payment | Common and legitimate |

| Pay Later Insurance | Coverage now, payment later | May involve financing or restrictions |

Many consumers are surprised to learn that the “deposit” and the “first premium payment” are not necessarily the same thing.

One of the biggest misconceptions in auto insurance involves the phrase “no deposit.” Insurance companies generally do not require security deposits in the same way landlords often do. Instead, they require payment toward the policy premium.

When an insurer advertises no-deposit insurance, they often mean:

Imagine an insurer offers a policy that costs $1,200 annually. The company may allow you to pay $200 today and then monthly installments afterward. The insurer may advertise this as low-down-payment insurance or no-deposit insurance because no separate deposit is charged. However, you still paid $200 before coverage started. That distinction is important.

Insurance is fundamentally a contract. The insurance company agrees to assume financial risk in exchange for premium payments. The moment coverage begins, the insurer becomes responsible for covered claims.

For example, if you obtain insurance at 10:00 AM and cause a serious accident at 11:00 AM, the insurer could immediately face thousands—or even hundreds of thousands—of dollars in potential liability. Because coverage starts immediately, insurers usually require payment before assuming that risk.

Without payment, there is often no valid insurance contract. This is why most reputable insurance companies require some form of payment before activating a policy.

The answer is simple: people search for it. Many websites, lead generation companies, and insurance marketers know consumers are looking for low-cost options.

In some cases, these advertisements lead to legitimate agencies. In other cases, they are simply collecting your information and selling leads to insurance companies. The wording may technically be legal, but it can create unrealistic expectations.

Whenever you see a claim that sounds too good to be true, request a written quote showing:

Seeing the actual numbers often reveals the reality behind the advertisement.

In practical terms, truly zero-upfront-payment car insurance is extremely rare. Most insurers require some payment before coverage becomes active. However, you may find options that reduce your upfront cost considerably.

A realistic option for drivers trying to reduce the amount due today.

Often lowers the first payment compared with paying the full policy upfront.

Sometimes available, but details and restrictions matter.

May spread premium payments, but fees and terms should be reviewed carefully.

These arrangements can reduce your upfront cost considerably. The important point is that low upfront cost and zero upfront cost are not the same thing.

The amount varies significantly depending on several factors. Insurance companies evaluate:

A driver with a clean record and a modest vehicle may pay far less upfront than someone with multiple accidents or violations.

| Policy Type | Annual Premium | Possible Initial Payment |

|---|---|---|

| Minimum Liability | $900 | $100-$200 |

| Standard Coverage | $1,500 | $150-$300 |

| Full Coverage | $2,400 | $250-$500 |

| High-Risk Driver | $3,000+ | $400-$800+ |

These examples are illustrations only. Actual premiums vary by state, insurer, driver profile, and coverage selections.

If your goal is to minimize upfront costs, focus on realistic strategies rather than searching endlessly for free insurance.

Shopping around remains one of the most effective ways to lower premiums. One company may quote $280 per month while another quotes $165 per month for similar coverage. Always compare at least five insurers before purchasing coverage. Even experienced insurance agents often recommend extensive comparison shopping because pricing differences can be substantial.

Paying monthly can reduce the amount due immediately. For example, paying in full might require about $1,200 upfront, while monthly billing may only require $150–$250 today, and some installment plans can lower the initial payment even more. Although monthly billing may cost slightly more over the life of the policy due to installment fees, it can dramatically reduce the initial payment.

Increasing your deductible can lower your premiums if you carry collision and comprehensive coverage. A $250 deductible usually means the highest premium, $500 is more moderate, and $1,000–$1,500 can lower your premium more. Remember that you’ll be responsible for the deductible amount if you file a claim. Only choose a deductible you could realistically afford.

Some coverages are optional and may increase your premium, such as rental reimbursement, roadside assistance, custom equipment coverage, and enhanced glass coverage. Removing optional features you do not need can help reduce both monthly costs and upfront payments.

Insurance companies often reward drivers who maintain continuous coverage. A lapse in coverage can lead to higher premiums, higher upfront payments, and fewer insurer options. Even a short lapse can increase costs, so maintaining uninterrupted coverage is one of the easiest long-term ways to save money.

While no major insurer consistently advertises true first-month-free coverage, several companies are frequently worth comparing when affordability is your priority.

Often competitive for online shoppers and drivers with clean records.

Frequently worth comparing for flexible coverage and higher-risk profiles.

Often competitive for drivers seeking a familiar national carrier.

Can be a useful comparison option depending on state and driver profile.

Worth reviewing for discounts, bundles, and payment options.

Often compared by drivers with violations or prior coverage issues.

Frequently considered by drivers who need nonstandard coverage.

Often markets flexible payment choices and low upfront options.

Can be worth comparing for drivers who need alternative options.

May offer competitive rates in states where available.

The cheapest company for one driver may be among the most expensive for another. This is why comparison shopping remains so important.

Not every low-cost insurance offer is legitimate. Watch for red flags such as:

Be careful with promises of approval regardless of circumstances.

Legitimate insurers usually require payment before coverage starts.

Requests for cryptocurrency or gift cards are major warning signs.

A real insurer should provide policy documents and payment records.

You should be able to identify the licensed insurance company.

Do not rush into a policy you cannot verify.

A legitimate insurer should clearly disclose policy terms, coverage limits, effective dates, premium amounts, and payment schedules. If you cannot verify these details, proceed cautiously.

Many drivers assume insurance prices are fixed, but there are several legitimate ways to reduce your initial payment and ongoing premiums.

| Discount Type | Potential Savings |

|---|---|

| Multi-Policy | Up to 25% |

| Multi-Vehicle | Up to 25% |

| Safe Driver | Varies |

| Good Student | Varies |

| Military | Varies |

| Defensive Driving Course | Varies |

| Automatic Payments | Small discount |

| Paperless Billing | Small discount |

| Telematics Program | Varies significantly |

Many insurers now offer telematics programs that monitor driving habits through a smartphone app or small device. These programs may evaluate braking habits, speeding, mileage, time of day driven, and phone use while driving.

If you drive fewer miles than average and have safe driving habits, telematics programs may help lower both your premium and future renewal rates.

Choosing the right amount of coverage is important. Some drivers purchase more coverage than they truly need, while others buy too little.

The goal is to find a balance between affordability and financial protection. For older vehicles with low market values, it may not make financial sense to carry extensive physical damage coverage. For newer financed vehicles, full coverage is usually required by the lender.

Never reduce liability coverage solely to lower your payment without understanding the financial risk. A serious accident can easily exceed state minimum requirements.

Many drivers searching for first-month-free insurance actually need something else: coverage immediately. Fortunately, same-day coverage is available from many insurers.

| Requirement | Purpose |

|---|---|

| Driver’s License | Verify identity |

| Vehicle VIN | Identify vehicle |

| Address | Determine rating territory |

| Driving History | Risk assessment |

| Prior Insurance Information | Underwriting |

| Payment Method | Activate coverage |

Most major insurers allow consumers to complete the process entirely online.

Yes. Many drivers believe a checking account is required to purchase insurance. That is generally not true. Depending on the insurer, payment options may include debit cards, credit cards, electronic payments, money orders in some situations, and agency payment arrangements. Accepted payment methods vary by company, so always verify payment options before starting the application process.

In many states, insurers may use credit-based insurance factors as part of their pricing models. Drivers with lower credit scores often face higher premiums, larger initial payments, and fewer carrier options. However, several states restrict or prohibit the use of credit information in insurance pricing.

The difference between insurers can be substantial, making comparison shopping especially important.

Drivers with speeding tickets, at-fault accidents, DUI convictions, SR-22 requirements, or suspended license history often pay more for coverage. The increased premium reflects the higher risk perceived by insurers.

In these situations, it becomes even more important to compare quotes from multiple companies. Some insurers specialize in higher-risk drivers and may provide more competitive pricing than standard carriers.

| Risk Factor | Impact on Premium |

|---|---|

| DUI | Very High |

| Multiple Tickets | High |

| At-Fault Accident | Moderate to High |

| Coverage Lapse | Moderate |

| Poor Driving History | High |

| Young Driver | Moderate to High |

Although these factors can increase costs, maintaining a clean driving record going forward usually helps reduce premiums over time.

Every state establishes minimum liability requirements. These laws determine the minimum amount of coverage drivers must carry. However, state minimum coverage does not necessarily provide adequate financial protection.

A major accident can quickly create high medical costs.

Modern vehicles can be expensive to repair or replace.

Claims can involve legal expenses and settlement risk.

Accidents may involve income-related damages.

Many insurance professionals recommend carrying limits above state minimum requirements whenever possible. While increasing limits may raise premiums slightly, it can provide significantly greater protection.

Liability-only coverage is often the least expensive insurance option available. It typically covers bodily injury liability and property damage liability. However, it generally does not cover damage to your own vehicle after an accident you cause.

| Feature | Liability Only | Full Coverage |

|---|---|---|

| Covers Your Vehicle | No | Yes |

| Covers Other Drivers | Yes | Yes |

| Lowest Premium | Yes | No |

| Lender Requirement | Usually No | Usually Yes |

| Upfront Cost | Lower | Higher |

If money is extremely tight, focus on realistic solutions rather than risky shortcuts.

Some states offer specialized programs designed to help lower-income drivers obtain legally required insurance coverage. Availability varies significantly by state.

Driving uninsured is usually far more expensive than purchasing insurance. Potential consequences can include fines, license suspension, vehicle impoundment, SR-22 filing requirements, increased future insurance costs, and personal liability for accident damages.

This distinction is one of the most important takeaways from this article. Many consumers search for “first month free car insurance,” but what they actually need is “low upfront payment car insurance.” These are very different concepts.

| Option | Legitimate? | Common? |

|---|---|---|

| First Month Free | Rarely | Uncommon |

| No Deposit | Sometimes misunderstood | Common |

| Low Down Payment | Yes | Very Common |

| Monthly Billing | Yes | Very Common |

| Premium Financing | Yes | Less Common |

The most realistic strategy for car insurance first month free no deposit is focusing on low upfront payments rather than expecting free coverage.

Following these steps can often save far more money than chasing questionable first-month-free advertisements.

The honest answer is that truly free first-month car insurance is extremely rare. Legitimate insurance companies generally require some form of payment before coverage begins.

When consumers search for “car insurance first month free no deposit,” they are often looking for affordable coverage with a low upfront cost. Fortunately, there are realistic ways to accomplish that goal.

You can often reduce your initial payment by:

The smartest approach is not searching endlessly for free insurance. The smartest approach is to find a reputable insurer that offers the best combination of affordability, coverage, and low upfront costs.

While truly free coverage is generally unrealistic, affordable coverage with a manageable first payment is often available if you are willing to compare quotes and understand how insurance billing works.

Compare first month free with low deposit options near you.

Start your quote and compare direct auto insurance rates in about five minutes.