Cheap Car Insurance in GA With No Down Payment

Company Trusted For Over 25+ Years*

Call us 1-855-371-6683

Company Trusted For Over 25+ Years*

If you need dirt cheap coverage, you’re probably searching for cheap car insurance in GA with no down payment. Due to increased rates in recent years, thousands of Georgia drivers are actively looking for cheaper coverage every month. Many Georgia drivers want to get covered with the lowest upfront costs.

The good news is that low-down-payment car insurance options do exist in Georgia. The bad news is that truly “no down payment” car insurance is often misunderstood. Most legitimate insurance companies require some form of initial payment before coverage begins. However, many insurers offer low down payments, low first payments, or flexible payment plans that can dramatically reduce your upfront costs.

The honest answer is usually no. Most licensed insurance companies require at least some payment before your policy becomes active.

This payment may be called:

Insurance companies assume financial risk the moment your policy begins. Because of this, they typically collect money before coverage starts. When most drivers search for “no down payment car insurance,” what they are actually looking for is:

Understanding this distinction can help you avoid misleading advertising and focus on finding the lowest amount due today.

Many advertisements use the phrase “no down payment” as a marketing term. In reality, most insurers are simply spreading payments differently.

Due Today: $250

Monthly Payment: $85

Due Today: $75

Monthly Payment: $110

Policy B appears more attractive because the upfront cost is lower. However, over six months, Policy B may actually cost more. This is why smart shoppers compare:

The cheapest policy is not always the one with the lowest first payment.

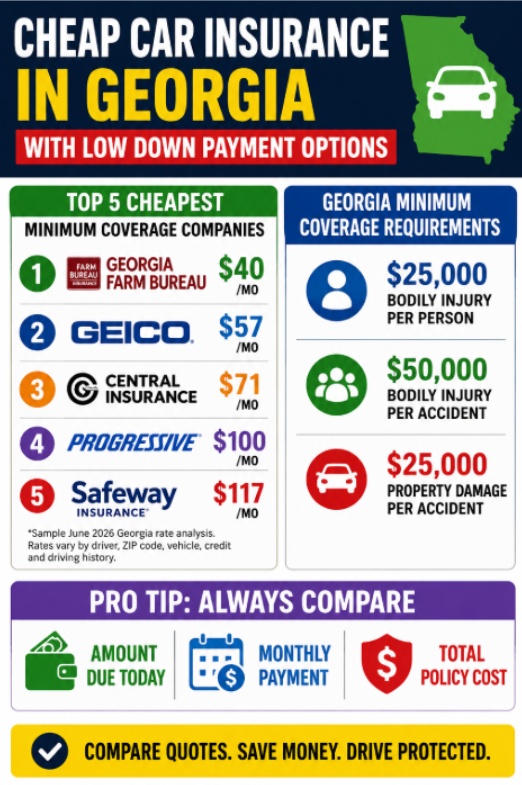

Georgia law requires all registered vehicles to carry liability insurance. For general background, vehicle insurance is the broader category that includes liability coverage, collision, comprehensive coverage, and other policy types. Current minimum requirements include:

$25,000 per person

$50,000 per accident

$25,000 per accident

25/50/25

These minimum limits satisfy Georgia law, but they may not provide enough protection in a serious accident.

For some drivers, yes. Minimum coverage may make sense if:

However, minimum coverage does not pay for damage to your own vehicle. If you finance or lease your vehicle, lenders typically require collision coverage and comprehensive coverage. These protections increase premiums but provide significantly more financial protection.

Many drivers focus only on the first payment and ignore the total six-month premium. Always compare the amount due today, monthly installments, and total policy cost before choosing coverage.

Usually, the cheapest legal option.

Benefits include:

Drawbacks:

Useful for:

Non-owner policies often cost less than traditional auto insurance.

Increase deductibles from:

This way, you can significantly lower premiums. However, you’ll pay more out of pocket after a claim.

No company is the cheapest for everyone. However, Georgia drivers frequently find competitive rates from:

![]()

Often among the lowest-cost insurers for Georgia residents.

Best for:

Known for competitive rates, a strong online experience, and good driver discounts.

Best for:

![]()

Frequently competitive for drivers with tickets, accidents, or those comparing multiple options.

Best for:

![]()

Often promotes low down payments and flexible payment plans.

Best for:

Focuses heavily on minimum coverage and low upfront payments.

Best for:

![]()

Frequently serves high-risk drivers and drivers rebuilding insurance history.

Best for:

![]()

Provides flexible payment structures.

Best for:

Young drivers should compare aggressively because rates vary dramatically.

The only way to know which company is cheapest for you is to compare quotes.

Georgia drivers with poor credit frequently pay substantially higher premiums than drivers with excellent credit. While insurers evaluate many factors, credit-based insurance scores often affect rates. Drivers with poor credit should compare multiple companies because the difference between insurers can be dramatic. Companies that are expensive for one driver profile may be surprisingly competitive for another.

Young drivers typically face some of the highest insurance premiums in Georgia. Limited driving history increases risk in the eyes of insurers.

Although Georgia does not require SR-22 filings for every violation, some drivers may need proof of financial responsibility after certain license or insurance-related issues.

Drivers who need SR-22-related coverage should compare multiple insurers because rates can vary significantly. Maintaining uninterrupted coverage becomes especially important in these situations.

| Rank | Company | Avg. Monthly Rate* | Best For |

|---|---|---|---|

| 🥇 | Georgia Farm Bureau | $40 | Cheapest minimum coverage |

| 🥈 | GEICO | $57 | Online quotes and discounts |

| 🥉 | Central Insurance | $71 | Regional value shoppers |

| 4 | Progressive | $100 | High-risk drivers |

| 5 | Safeway | $117 | Alternative options |

Atlanta-area drivers often pay more because of traffic density, accident frequency, theft risk, and repair costs.

Smaller towns and rural areas may have lower average premiums.

ZIP code changes can sometimes impact rates more than vehicle changes.

This is why two drivers with identical records may receive dramatically different quotes.

Check your own situation before choosing a policy. The cheapest option for one Georgia driver may not be the cheapest or safest option for another.

| Driver Situation | Best Starting Point | Why |

|---|---|---|

| Need cheapest legal coverage |

State minimum liability | Usually lowest upfront cost |

| Financed vehicle | Full coverage | Lender usually requires comprehensive and collision |

| Poor credit | Compare Georgia Farm Bureau, GEICO, Progressive | Pricing varies heavily by company |

| Recent ticket | Compare Progressive, GEICO, State Farm | Some insurers penalize tickets less |

| Prior lapse | Compare high-risk carriers | Lapses can raise deposits and premiums |

| Young driver | Parent policy if possible | Usually cheaper than separate coverage |

| No checking account | Debit or credit card payment | Many insurers accept card payments |

This is the biggest money-saving strategy. Getting 3–5 quotes can save hundreds annually.

If your vehicle has little value, minimum coverage may significantly reduce upfront costs.

Coverage lapses often increase premiums and required deposits.

Credit can influence insurance pricing in many situations. Improving your credit score may reduce premiums over time.

Atlanta drivers face unique challenges. Factors increasing rates include:

Because of these factors, Atlanta drivers often pay more than drivers in smaller Georgia cities. Neighborhoods can significantly impact pricing.

Drivers in Sandy Springs, Marietta, Decatur, College Park, and East Point may see different rates despite having identical driving records. Atlanta drivers should compare quotes every renewal period.

Savannah drivers benefit from lower traffic levels than Atlanta. However, tourism traffic, coastal weather risks, and hurricane exposure can affect rates.

Augusta often offers lower average premiums than Atlanta. Important factors include commuting patterns, military households, and vehicle usage.

Columbus drivers frequently compare GEICO, Progressive, State Farm, and Georgia Farm Bureau. Military families may qualify for additional savings opportunities.

Macon often provides opportunities for lower premiums compared to larger metropolitan areas. Still, rates depend heavily on driving history, vehicle type, credit profile, and coverage level.

Need coverage today? Many insurers provide same-day coverage. The process usually takes:

Many companies can activate policies within minutes.

Modern vehicles cost more to repair.

Accident-related medical expenses continue rising.

Atlanta remains one of the busiest traffic markets in the Southeast.

Insurance companies factor lawsuit risks into pricing.

Parts, labor, and vehicle replacement costs have increased significantly.

One speeding ticket can increase rates substantially. Progressive and State Farm often remain competitive.

Accidents can raise premiums for years. Comparing quotes becomes even more important after an accident.

Poor credit frequently increases insurance costs. Some insurers penalize poor credit more heavily than others.

Lapses often trigger higher rates, higher deposits, and fewer available options. Avoiding lapses is one of the easiest ways to save money.

Many drivers focus only on today’s payment. That can be a mistake.

Pros:

Cons:

Pros:

Cons:

The best option depends on your cash flow and financial situation.

Avoid companies promising:

Insurance companies do not provide free coverage.

Always verify coverage directly with the insurer.

Legitimate companies provide policy documents and payment records.

Verify licenses through Georgia insurance resources.

Don’t focus only on the amount due today. Many low-down-payment policies cost more over six months. Always compare the first payment, monthly premium, and total policy cost before choosing coverage.

Cheap car insurance in GA with no down payment is best understood as finding the lowest possible upfront payment while maintaining legal coverage. True zero-down insurance is rare, but many Georgia drivers can dramatically reduce their first payment by comparing quotes, choosing appropriate coverage levels, maintaining continuous insurance, and exploring flexible payment plans.

The smartest shoppers compare three numbers:

Do that consistently, and you’ll put yourself in the best position to find affordable Georgia car insurance without overpaying. For drivers searching for cheap car insurance in GA with no down payment, comparing several quotes is the safest way to find a low upfront cost without choosing a weak policy.

Compare the cheapest car insurance plans in Georgia with no down payment.

Start your quote and compare your custom rates in about five minutes. Save more today with direct GA auto insurance rates.