Non-Owner Car Insurance in Florida

Company Trusted For Over 25+ Years*

Call us 1-855-371-6683

Company Trusted For Over 25+ Years*

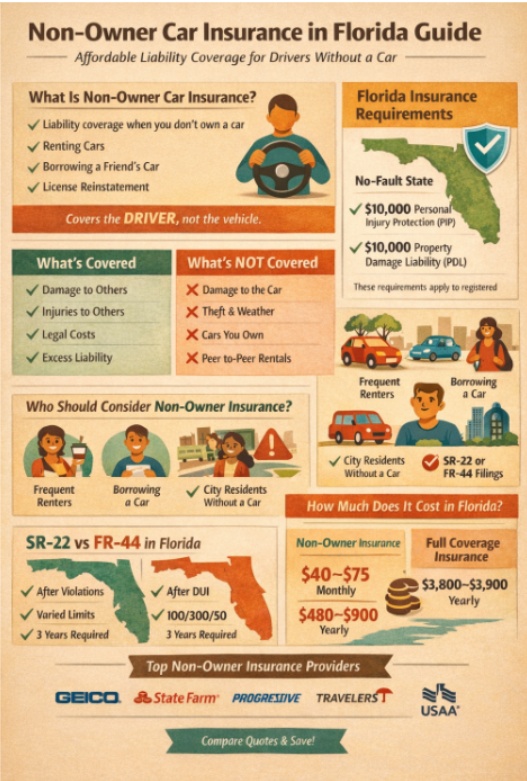

Non-owner car insurance in Florida is a type of auto insurance for licensed drivers who do not own a vehicle but still need liability coverage when they drive. It’s most commonly used for borrowing a friend’s car, renting vehicles, or maintaining continuous insurance coverage for future pricing advantages.

Florida can be a really high-risk place to drive. Traffic is heavy in metro areas like Miami, Orlando, Tampa, and Fort Lauderdale. The Sunshine State also has a large share of uninsured drivers compared to many other states, which increases the odds that a crash turns into a financial mess. For drivers who don’t own a car, non-owner auto insurance in FL is often the cheapest legitimate way to stay protected and avoid a coverage gap.

Non-owner car insurance is a liability-focused policy that follows the driver instead of insuring a specific vehicle. If you cause an accident while driving a car you do not own (and you have permission to use it), your non-owner policy can help pay for the other person’s losses.

Most Florida non-owner policies are built around these coverages:

Florida is known as a “no-fault” state because many injury-related expenses after a crash are handled through Personal Injury Protection (PIP) regardless of fault. Florida requires vehicles registered in the state to maintain at least $10,000 in PIP and $10,000 in Property Damage Liability (PDL). That requirement is tied to vehicles and registration, not automatically to every person who holds a Florida license.

Because a non-owner policy does not insure a specific registered vehicle, PIP on a non-owner policy is not universal. Some insurers can structure non-owner coverage that includes PIP in Florida, while others will not. If PIP matters to you, you must ask directly and get the details in writing.

When you borrow a car, the owner’s insurance is usually the first policy that responds to a claim. If a loss exceeds the owner’s liability limits, a non-owner policy may provide secondary or excess liability coverage depending on the policy language and the facts of the crash.

Non-owner coverage is usually a good fit in Florida if you drive occasionally but don’t own a car. It is especially common for:

If you rent cars multiple times a year, non-owner insurance can be a cost-effective way to maintain ongoing liability protection rather than purchasing liability coverage each time you rent.

If you occasionally borrow a friend’s or relative’s car, non-owner insurance can protect you if you cause an accident and the damages go beyond the owner’s limits.

Many insurers price policies partly based on whether you have had continuous insurance. A non-owner policy can keep you insured even when you don’t own a vehicle, helping you avoid a gap that could raise your future premiums.

If your license is suspended and Florida requires proof of financial responsibility, a non-owner policy may be an option to meet the requirement and get reinstated.

If you live in a dense area and rely on public transit, rideshare, or walking, but still drive occasionally, non-owner insurance may be the simplest way to stay protected.

This is the part that causes the most surprises, so it’s worth being blunt.

Non-owner insurance usually does not cover:

No collision coverage. No comprehensive coverage. If you damage the vehicle, that’s typically handled through the owner’s policy, a rental company’s options, or out of pocket.

Those are comprehensive-type claims, and non-owner insurance is not built for them.

If you have a vehicle you drive frequently, even if it is not yours on paper, insurers often consider that regular access, and a non-owner policy may not apply.

Peer-to-peer services like Turo are not the same as traditional car rentals. Some personal policies exclude peer-to-peer rentals, while platforms may provide separate protection plans for trips. You should verify exactly what applies before you drive.

Florida uses SR-22 and FR-44 filings to make sure certain high-risk drivers maintain required insurance.

|

SR-22 in Florida

Usually required for

Serious insurance-related or driving-related issues, such as driving uninsured, certain crashes, or license suspensions tied to insurance lapses. Coverage requirement

Limits depend on the reason for suspension. Required limits

10 / 20 / 10 Typical filing period

3 years |

FR-44 in Florida (DUI)

Usually required for

Certain DUI convictions. Coverage requirement

Higher liability limits than SR-22. Required limits

100 / 300 / 50 or350,000 CSL Typical filing period

3 years |

A non-owner policy can sometimes satisfy SR-22 or FR-44 requirements if the insurer offers the filing and the policy is written with the required limits. Not every company will offer FR-44 on a non-owner policy, so you have to ask directly.

Non-owner insurance costs vary, but it is usually far cheaper than full coverage auto insurance in Florida.

As a practical late-2025 range, many clean drivers see non-owner rates around $40 to $75 per month, which comes out to roughly $480 to $900 per year, depending on location, age, and chosen limits. Rates rise for violations, accidents, poor credit-based insurance scores, and required SR-22 or FR-44 filings.

In general, Florida full coverage premiums are several times higher than non-owner liability-only coverage, which is why non-owner insurance is popular for low-mileage drivers who do not own a car.

Availability changes by ZIP code and driver profile, but these are commonly strong options for Florida non-owner coverage:

GEICO is often one of the lowest-cost options and commonly used for SR-22 filings.

GEICO is often one of the lowest-cost options and commonly used for SR-22 filings.

![]() State Farm is strong for drivers who prefer working with local agents and want help navigating filings.

State Farm is strong for drivers who prefer working with local agents and want help navigating filings.

![]() Progressive is often more flexible for higher-risk situations, including drivers who need elevated limits.

Progressive is often more flexible for higher-risk situations, including drivers who need elevated limits.

![]() Travelers is frequently competitive for experienced drivers, with a solid service reputation.

Travelers is frequently competitive for experienced drivers, with a solid service reputation.

![]() Allstate can be competitive in some areas.

Allstate can be competitive in some areas.

![]() USAA can be excellent pricing for those eligible (military members and families).

USAA can be excellent pricing for those eligible (military members and families).

Not every insurer markets non-owner insurance online, so you may need to call and ask specifically for a “non-owner” or “named operator” policy.

Buying a non-owner policy is usually straightforward, but it often takes a phone call.

A clean process looks like this:

Once you purchase the policy, proof of insurance and any required SR-22/FR-44 filing is often issued quickly, sometimes the same day.

Non-owner car insurance is one of the best ways for Florida drivers without a car to stay insured, avoid coverage gaps, and protect themselves from liability claims. It is especially useful for renters, occasional drivers, and people who need SR-22 or FR-44 filings but do not own a vehicle.

If you want the best deal, compare multiple quotes, confirm whether PIP is available, and make sure the policy fits how you actually drive. Done correctly, non-owner car insurance in Florida can save you hundreds per year while keeping you protected on Florida roads. Compare non-owner auto insurance quotes in Florida in under 5 minutes and save more with direct rates.